Market & Legal Update

September 2022

Market Update | Market Turmoil Continues Behind the Fed’s Aggressive Stance

Markets continued to decline in September following the Federal Reserve’s assertion of their aggressive stance in Jackson Hole at the end of August. The month of September did not offer much relief as inflation levels remained elevated and the Federal Reserve enacted another 0.75% rate hike, while confirming future rate increases are likely on the horizon. 13 of the 21 trading days in September were negative, sending all 3 major US Indices into a bear market and marking the third consecutive quarter of declines. The Dow Jones Industrial Average (DJIA) decreased 22% from its January highs and finished September down 8.8% month-to-date. The S&P 500 declined 9.2% in September, while the index has experienced intraday losses of 1% or more 50 times so far this year, representing the most downside volatility since 2009. The tech-heavy NASDAQ finished down 10.5% in September, while equities also struggled abroad, as the MSCI EAFE Index finished down 9.3% for the month.

| Market Return Indexes | September 2022 | Q3 2022 | YTD 2022 |

|---|---|---|---|

| Dow Jones Industrial Average | -8.8% | -6.7% | -21.0% |

| S&P 500 | -9.2% | -4.9% | -23.9% |

| NASDAQ (price change) | -10.5% | -4.1% | -32.4% |

| MSCI Eur. Australasia Far East (EAFE) | -9.3% | -9.3% | -26.8% |

| MSCI Emerging Markets | -11.7% | -11.4% | -26.9% |

| Bloomberg High Yield | -4.0% | -0.7% | -14.7% |

| Bloomberg U.S. Aggregate Bond | -4.3% | -4.8% | -14.6% |

| Yield Data | September 2022 | August 2022 | July 2022 |

| U.S. 10-Year Treasury Yield | 3.83% | 3.15% | 2.67% |

Despite a large drop in energy prices, the release of August inflation results revealed only a slight decrease in CPI (Consumer Price Index) from 8.5% in July to 8.3%. Within the Headline CPI data, increases in the shelter, food, and medical care indexes were the largest. These increases were mostly offset by a 10.6% decline in the gasoline index, as well as decreases across airline fares, communication, and used cars and trucks, but not enough to bring inflation down in a meaningful way.

While the CPI downtrend is welcomed, Core CPI, an inflation measure which excludes volatile food and energy prices, increased from 5.9% in July to 6.3% in August. The shelter index rose 6.2%, accounting for about 40% of the total increase within the Core CPI measure. Other indexes with notable increases include household furnishings and operations (+9.9%), medical care (+5.4%), new vehicles (+10.1%), and used cars and trucks (+7.8%). The increase in this measure is certainly concerning and suggests that the U.S. has a long road ahead before it can tackle its inflation problem. Due to the increase in Core CPI, as well as the elevated levels of CPI, the Federal Reserve reiterated their aggressive stance and determination to combat inflation during the September FOMC meeting.

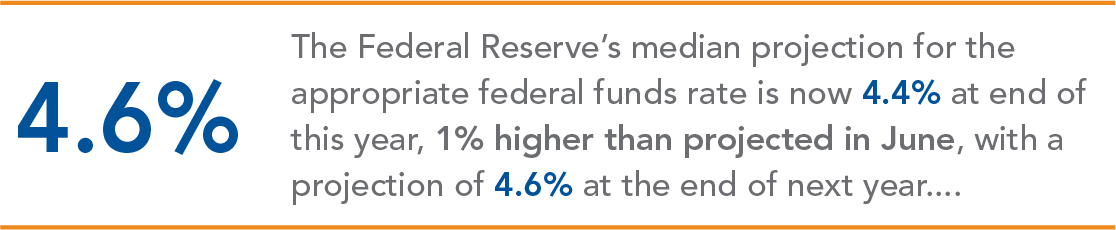

Federal Reserve Chairman Jerome Powell spoke following the FOMC’s September meeting, where he announced a unanimous vote to approve a 0.75% increase in the primary credit rate to 3.25%. Powell announced that the FOMC anticipates ongoing increases in the target range will be appropriate. The Federal Reserve’s median projection for the appropriate federal funds rate is now 4.4% at end of this year, 1% higher than projected in June, with a projection of 4.6% at the end of next year, diminishing hopes that rates will begin to decline in 2023. Since June, FOMC participants have marked down their projections for economic activity, which now sit well below the estimates of longer-run normal growth rates, showing the potential impact of the Federal Reserve’s tightening on the U.S. economy.

The Federal Reserve continues to cite the tight labor market as one of the justifications behind its hawkish view. Job gains have been strong, as total nonfarm payroll employment increased by 315,000 in August, which have now risen by a total 5.8 million over the past 12 months, as the labor market continued to recover from the job losses of the pandemic-induced recession. This growth brings total nonfarm employment 240,000 higher than its pre-pandemic level in February 2020. September also revealed a welcomed uptick in the labor force participation rate to 62.4% as of August, which is a measure that must increase to stabilize the worker supply issues within the labor market. August did however see the year’s first increase in the unemployment rate, which rose 0.2% to 3.7%. The FOMC’s median projection for the unemployment rate increased to 4.4% for the end of next year, with the median rate running above the longer-run normal level over the next 3 years. Although job growth has been robust this year, Americans are bracing for impact within the labor market, as the consequences of the Federal Reserve’s economic tightening have yet to be truly seen.

The Federal Reserve has not been shy about confirming the concerns of both American citizens and markets, as Charmain Powell noted in September that restoring price stability will “likely require maintaining a restrictive policy stance for some time” as well as “a sustained period of below-trend growth, and there will very likely be some softening of labor market conditions.” The Federal Reserve’s aggressive stance with no end to rate hikes in sight, and the ongoing threat to the labor market continues to turn markets downward through the month of September. Markets will look for any signs of inflation relief, which will allow the Federal Reserve to begin easing its tightening of the U.S. economy.

Legal Update | Qualified Birth or Adoption Distributions (QBADs)

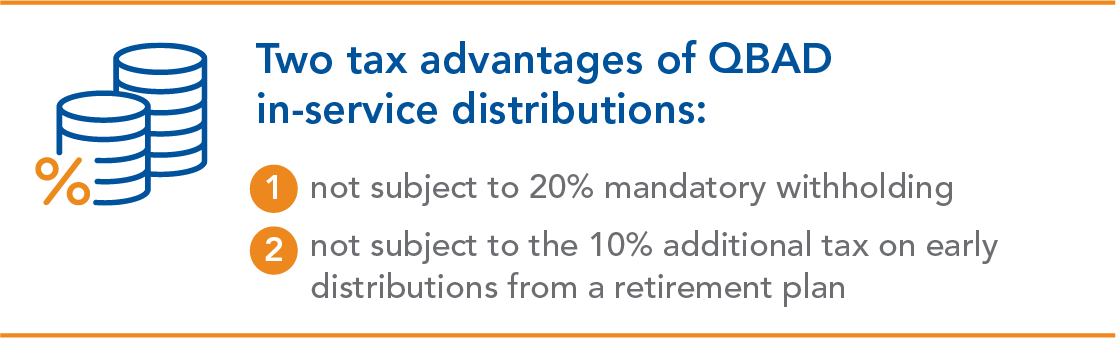

The Setting Every Community Up for Retirement Act of 2019 (“SECURE Act”) introduced a new in-service distribution option available to certain defined contribution plans known as the Qualified Birth or Adoption Distribution ("QBAD"). Under this optional provision, defined contribution plans (401(a), 401(k), 403(b) or governmental 457(b) plans) can provide plan participants with the opportunity to elect an in-service distribution of up to $5,000 to assist with expenses in connection with the birth or adoption of a child. Two tax advantages of QBAD in-service distributions are that they are not subject to 20% mandatory withholding and are not subject to the 10% additional tax on early distributions from a retirement plan; however, they are still included in gross income. QBADs were permissible as an optional distribution, at the discretion of the plan sponsor, beginning January 1, 2020.1

Many plans have either recently added QBADs or are considering adding QBADs to give their employees an opportunity to reduce some of the financial burdens associated with becoming parents. Whether your plan currently allows QBADs or you’re considering adding QBADs, the following Q&As from IRS Notice 2020-68 provide additional information regarding these distributions.

What is a QBAD?

The Notice defines a QBAD as a distribution of up to $5,000 from an eligible defined contribution plan to a participant if the distribution is made during the 1-year period beginning on the date on which the participant’s child is born or on the date the participant’s legal adoption of a child has been finalized.

Can a QBAD be repaid to the plan?

Yes. A participant may recontribute any portion of a QBAD up to the entire amount of the distribution but is not required to recontribute any amount distributed. The recontribution amount may not exceed the aggregate

amount of all QBADs made to the participant and the recontribution must be made to a plan in which the individual is a beneficiary and to which a rollover can be made. It does not appear that a participant owes the plan any interest on the recontribution amount.

A plan cannot refuse the recontribution of a QBAD if the plan permits QBADs, the participant received the QBAD from that plan and the participant is eligible to make a rollover contribution to the plan at the time of the requested recontribution. Additionally, the recontribution can generally be made at any time, as it is not subject to the 60-day time limit for other rollovers.

What are QBAD requirements?

A QBAD requires that the child or adoptee be identified by name, age and taxpayer identification number on the participant’s tax return for the taxable year in which the QBAD is made.

An eligible adoptee for purposes of a QBAD is any individual who has not attained age 18 or who is physically or mentally incapable of self-support. An eligible adoptee does not include the child of the participant’s spouse. To be considered “physically or mentally incapable of self-support,” an adoptee must be “unable to engage in any substantial gainful activity by reason of any medically determinable physical or mental impairment that can be expected to result in death or to be of long-continued and indefinite duration.”

What are the limits on how many QBADs a family can obtain?

Each parent may receive a QBAD with respect to the same child or adoptee. In addition, a participant is permitted to receive a QBAD with respect to the birth or adoption of more than one child if the distributions are made during the 1-year period following the date on which the children are born or legally adopted. For example, if the legal adoption of one child is finalized in the same year as the participants become parents to twins, then the parents are each eligible for QBADs up to $15,000 if they otherwise meet the requirements for the QBADs.

What information must the plan administrator have to issue a QBAD?

A plan administrator or plan sponsor may rely on the reasonable representations from a participant regarding the request for a QBAD, unless the plan sponsor or plan administrator has actual knowledge to the contrary.

If a plan doesn’t permit QBADs, can a participant treat an otherwise allowable in-service distribution as a QBAD?

Yes. If a participant receives an otherwise permissible in-service distribution that also meets the requirements of a QBAD, the participant may treat the distribution as a QBAD on the participant’s federal tax return.

More Guidance Expected

While Notice 2020-68 answers many questions regarding QBADs, more guidance from the IRS is expected. For example, will the IRS require that voluntary recontributions of QBADs be made in a particular way, that is, in a single lump sum, or through payroll deductions or via another payment form to the plan? Does a QBAD affect a requested hardship distribution or a loan under the plan – or vice versa? At this point, without further IRS guidance, it appears that recontributions or repayments (without interest) may be made in any way that the plan administrator considers reasonable.

How USI Consulting Group Can Assist

USI Consulting Group (USICG) consultants can help you with your plan design and determining whether QBADs and/or other optional distributions fit your objectives. In addition, USICG will monitor SECURE Act guidance issued by the IRS to ensure that you are fully and timely informed of the current requirements for your plan’s QBADs.

Retirement Resources for You

The USI Consulting Group team is happy to assist employers with all retirement plan compliance matters and changes in the market, including those discussed here, to help you mitigate risk and financial impact to your organization.

Questions? Contact your USICG representative, visit our Contact Us page or reach out to us directly at information@usicg.com.

For USI Consulting Group Service Regions please click here.

For previous market and legal commentaries please click here.

1 See August 2022 Market & Legal Update regarding deadlines to formalize required and optional provisions under the SECURE Act.

This information is provided solely for educational purposes and is not to be construed as investment, legal or tax advice. Prior to acting on this information, we recommend that you seek independent advice tax advice specific to your situation from a qualified investment/legal/tax professional.

An index is a measure of value changes in a representative grouping of stocks, bonds, or other securities. Indexes are used primarily for comparative performance measurement and as a gauge of movements in financial markets. You cannot invest directly in an index and, for comparative purposes; they do not reflect the effect of the various fees inherent in actual investment vehicles.

The S&P 500 Index is a market value weighted index showing the change in the aggregate market value of 500 U.S. stocks. It is a commonly used measure of stock market total return performance. The Dow Jones Industrial Average is a price weighted index comprised of 30 actively traded blue chip stocks; primarily industrial companies, but including some service oriented firms. The NASDAQ Composite Index is a market-value weighted index that measures all domestic and non-U.S. based securities listed on the NASDAQ Stock Market. Gross Domestic Product (GDP) is the market value of the goods and services produced by labor and property in the U.S. It is comprised of consumer and government purchases, net exports of goods and services, and private domestic investments. The Commerce Department releases figures for GDP on a quarterly basis. Inflation adjusted GDP (or real GDP) is used to measure growth of the U.S. economy.

The MSCI Europe and Australasia, Far East Equity Index (EAFE) is a market capitalization weighted unmanaged index developed by Morgan Stanley Capital International to measure approximately 1,100 securities in 21 major overseas stock markets. It is a commonly used measure for foreign stock market performance. The Barclays Capital U.S. Aggregate Index covers the U.S. Dollar denominated investment grade, fixed-rate, taxable bond market of SEC-registered securities. The Barclays Capital U.S. Corporate High Yield Index covers the U.S. Dollar denominated, non-investment grade, fixed income, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s Fitch, and S&P is Ba1/BB+/BB+ or below. The MSCI Emerging Markets Index (EM) is a free-float-adjusted market-capitalization index developed by Morgan Stanley Capital International. It is designed to measure the equity market performance of 26 emerging market countries.

The 10 Year Treasury Yield is the interest rate the U.S. government pays to borrow money for a 10-year period. In addition to influencing how much the government pays to borrow over this time-frame, the 10-year Treasury Yields also determines how much investors earn by investing in this debt and it is a good indicator of investor sentiment The higher the yield, the better the economic outlook.

Market Update is a monthly publication circulated by USI Advisors, Inc. and is designed to highlight various market and economic information. It is not intended to interpret laws or regulations. This report has been prepared solely for informational purposes, based upon information generally available to the public from sources believed to be reliable, but no representation or warranty is given with respect to its completeness.

This report is not designed to be a comprehensive analysis of any topic discussed herein, and should not be relied upon as the only source of information. Additionally, this report is not intended to represent advice or a recommendation of any kind, as it does not consider the specific investment objectives, financial situation and/or particular needs of any individual client.

Investment Advice provided by USI Advisors, Inc. Under certain arrangements, securities offered to the Plan through USI Securities, Inc. Member FINRA/SIPC.

USI Consulting Group is an affiliate of both USI Advisors, Inc. and USI Securities, Inc.

5022.S1003.0054

RECENT PUBLICATIONS

- June 2026 | Market & Legal Update 7/6/2026

- May 2026 | Market & Legal Update 6/3/2026

- April 2026 | Market & Legal Update 5/4/2026

Not receiving our newsletter?

Stay up to date with retirement plan updates and insights by subscribing to our email list.