Retirement Insights

Reduce Future Volatility: Lock in Funded Status Gains

November 17, 2022

While the rising rate environment of 2022 has created an incredibly volatile environment for the capital markets, it has also opened the best window of opportunity in several decades to review and adjust the fixed income investments of a pension plan’s portfolio.

Most common investment allocations that focus solely on assets can produce significant year-over-year variation in funding levels and contribution requirements. That approach can often lead to suboptimal investment and corporate finance results. Integrating actuarial and investment management for your pension plan’s governance enables you to optimize your funding levels and move forward with less volatile results.

Take Advantage of This Opportunity

Despite tremendous equity gains over the past decade, pension plan sponsors were not able to generate funded status advances as declining rates prevailed during those years. That environment has changed, with rates increasing at a record pace and liabilities plummeting. Over the past 18 months, there has been a substantial increase in the funded status of pension plans.

Market conditions are incredibly favorable for any de-risking activity related to the recent increase in rates: Now may be the time to lock in some of these funded status gains, and at the same time hedge that liability exposure prospectively by reallocating the fixed income assets to a liability driven investment (LDI) portfolio.

This re-adjustment provides a tremendous de-risking opportunity without negatively impacting the plan’s expected rate of return. The key is an integrated approach of actuarial services and investment advice which allows pension plan sponsors to set an investment strategy that recognizes their plan’s current and potential future funded status.

It’s Time to Consider an LDI Strategy

Strategic de-risking monitored by an experienced integrated actuarial and investment advisory team helps retirement plan fiduciaries make decisions confidently and mitigate risk. As 2022 draws to a close, plan sponsors may benefit from the rising rate environment as the hedge ratio can be increased significantly without adversely impacting the expected rate of return.

While asset values are down, funded ratios have, in general, improved due to the significant increase in interest rates. For plan sponsors who have portfolios unaligned with the plan’s liabilities, a shift in their fixed income allocations to an LDI strategy could dramatically reduce volatility without impacting their expected returns.

For example, many pension plans use a standard 60% equity and 40% fixed income portfolio, while an LDI strategy may use a 60% equity and 40% custom LDI mandate. The LDI approach can dramatically improve hedging properties of the portfolio and decrease funded status volatility without impacting the portfolio’s expected rate of return. Depending on the execution of the strategy, an LDI-mandate approach may result in doubling or tripling the hedging benefits of the portfolio, compared to a traditional fixed income portfolio consisting of core intermediate-term bonds.

Implementing an LDI strategy allows plan sponsors to lock in their funded status gains and better preserve them going forward. The timing may also be right for evaluating other de-risking activities such as annuity purchases and lump sum windows. Employers can experience optimal results through an integrated actuarial, investment and annuity consulting team that tailors a solution that meets the unique needs of their plan.

Effectiveness of an Integrated Approach

Employers should rely on a team of actuarial consultants and investment advisors who work together to design an efficient asset allocation and contribution strategy that achieves corporate plan objectives while optimizing funded status variability.

USI Consulting Group (USICG) has the expertise, resources and bench strength to assist pension plan sponsors and committees manage both assets and liabilities, while mitigating risk. Integrated services are at the heart of our client solutions and USICG’s experts utilize this approach to develop a comprehensive LDI strategy that meets each plans sponsor’s unique needs and plan goals.1 This approach includes implementing a contribution plan and incorporating additional de-risking tools such as annuity purchases or lump sum windows as appropriate.

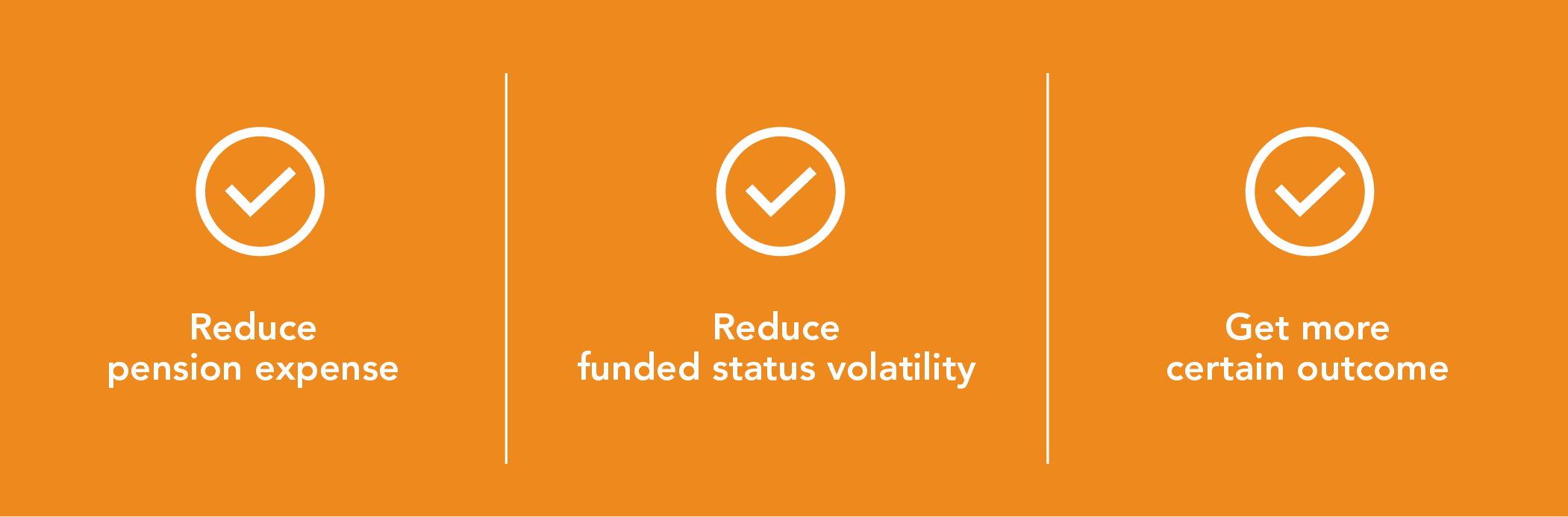

USICG’s integrated approach to implementing an LDI strategy helps:

The actuary and investment consultant work jointly on a thoughtfully constructed LDI solution to:

Benefit from an Integrated Approach with an Experienced Team

USICG’s integrated asset and liability management process helps employers make confident decisions and mitigate risk. Our team of more than 80 in-house actuaries and more than 60 in-house investment advisory representatives offers these advantages:

- Pension plan governance expertise with assets and liabilities

- One integrated team with thorough knowledge of your entire plan

- A single point of contact for actuarial and investment advisory services, which saves time and resources

- Increased fiduciary oversight – one contact which makes it easier to stay informed and take timely action

- Total fee reductions up 25% to 50% compared to firms with similar resources

- Mutual alignment of interests for the retirement plan’s needs, instead of using a siloed approach

How USI Consulting Group Can Help

USICG’s team of investment advisory and actuarial consultants provides a holistic, integrated approach to meeting the goals of our clients. If you are interested in learning how your organization can benefit from an integrated LDI strategy, contact your local USICG representative, visit our Contact Us page or reach out to us directly at information@usicg.com.

![]()

1 Investment Advice provided to the Plan by USI Advisors, Inc. Under certain arrangements, securities offered to the Plan through USI Securities, Inc. Member FINRA/SIPC. Both USI Advisors, Inc. and USI Securities, Inc. are affiliates of USI Consulting Group.

This information is provided solely for educational purposes and is not to be construed as investment, legal or tax advice. Prior to acting on this information, we recommend that you seek independent advice specific to your situation from a qualified investment/legal/tax professional. | 1022.S1113.0080

INSIGHTS BY TOPIC

Not receiving our newsletter?

Stay up to date with retirement plan updates and insights by subscribing to our email list.