Retirement Insights

WHITE PAPER: Financial Wellness

It’s Time to Tend to Your Employees’ Financial Health

July 29, 2022

In this article:

- Financial Well-being and Your Employees' Health

- Impact of Financial Well-being on Mental and Physical Health

- Impact of Financial Well-being on an Organization

- Four Ways Investing in Financial Empowerment Can Make a Difference

- Where Do We Go From Here?

Financial well-being and your employees’ health

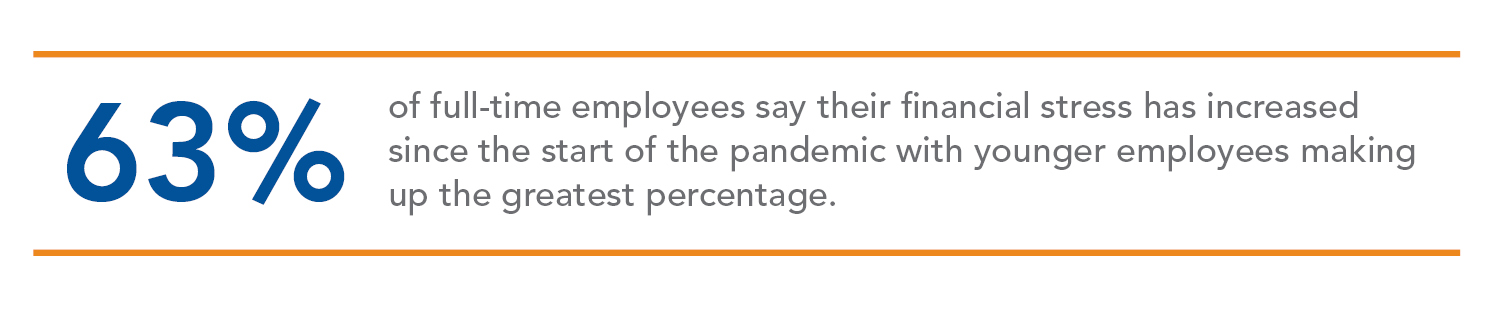

Entering into the third year of the COVID-19 pandemic, the lives of workers across the country have been disrupted in a number of ways. Employers have taken measures to reduce costs, including making layoffs, reducing salaries and cutting back on other benefits. This has resulted in a profound negative impact on both employers and employees, as several studies suggest that finances are the top cause of employee stress. According to the 2022 PwC Employee Financial Wellness Survey, 63% of full-time employees say their financial stress has increased since the start of the pandemic with younger employees making up the greatest percentage. Headlines about the virus are now being replaced with concerns over inflation, which has caused new financial challenges to employees.

Financial well-being can have a significant impact on mental and physical health. Employees who worry about their financial well-being may have a hard time being fully present at work. Employees may be experiencing financial difficulties that create anxiety, guilt and even fear in the workplace regardless of income level or financial education. These feelings are often hidden but can manifest themselves via stress, workplace distractions, decreased engagement, employee burnout or long-term mental and physical health concerns.

According to the Money and Mental Health Policy Institute, mental health problems can affect expenditures and the ability to save. Many people with mental health challenges report that their spending patterns and ability to make financial decisions change significantly, with a recent study showing 63% find it difficult to make financial decisions and 38% took out a loan that they would not otherwise have taken out.

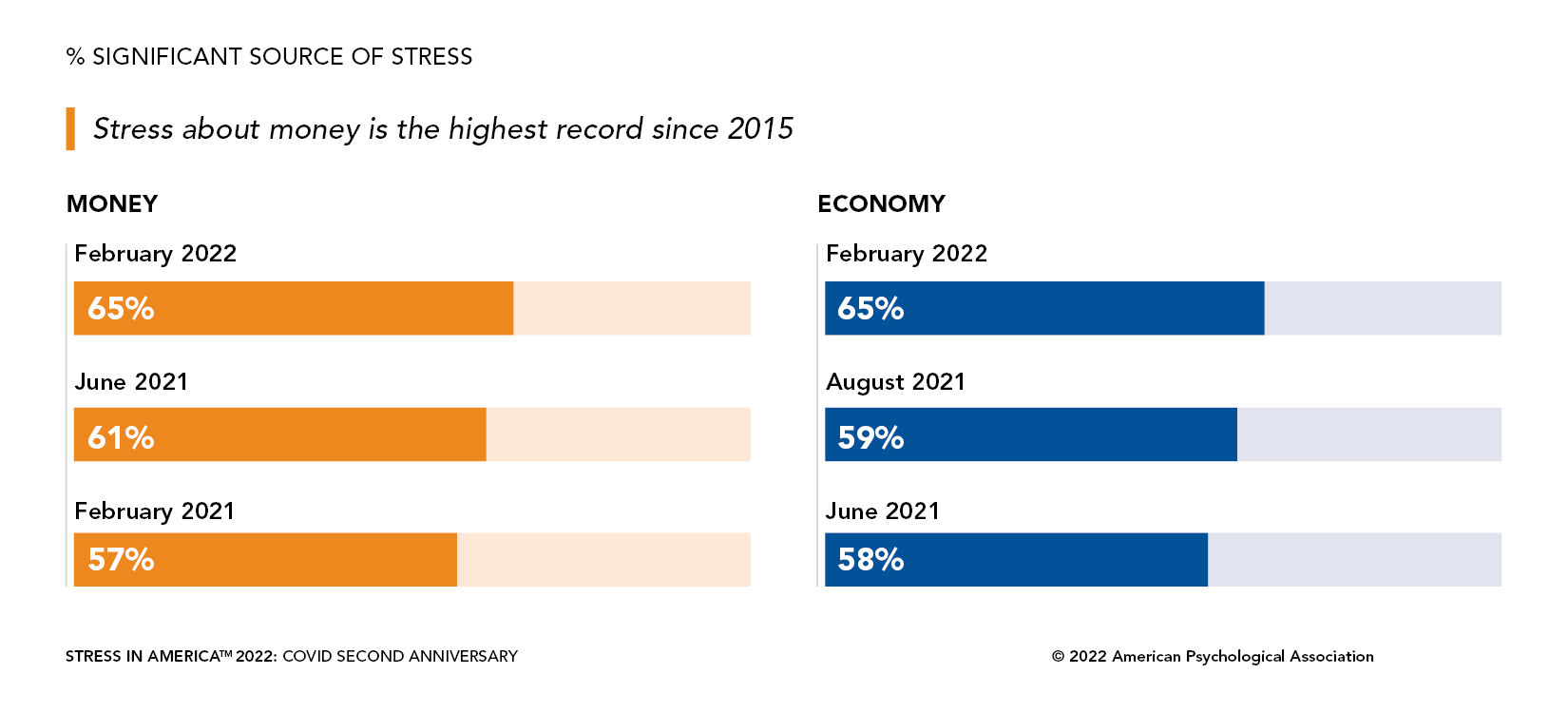

Another recent study from the American Psychological Association revealed that stress about money is the highest recorded since 2015. 65% of adults noted money as a source of stress. The impact of the pandemic over the last few years has only exacerbated the issue for American workers.

There are clear impacts to the organization as a result. Employees may reduce or stop contributing to workplace savings programs, resulting in delayed retirements. There can be increased healthcare costs and worker compensation claims. Distracted employees can be less productive at work, resulting in absenteeism or worse, presenteeism. The impact to an organization’s bottom line may not be noticeable in the short-term but can compound to have a dramatic impact over several years. The good news is these negative impacts can be reduced by implementing a robust financial wellness program.

While business leaders do not have an obligation to address the financial wellness of their employees, they do stand to benefit by taking the problem head on.

Here are four ways investing in the financial empowerment of your employees can make a difference in your business:

Employee Hiring and Retention

In 2021, according to the U.S. Bureau of Labor Statistics, over 47 million Americans voluntarily quit their jobs which is now widely being called the Great Resignation. Three things motivated employees to leave a job; leadership, pay and growth opportunities. Although your hands might be tied in the amount of additional pay you can provide an employee given the scope and function of their role, you can certainly help an employee feel more confident with their current salary by addressing issues that may make them think it’s just not enough. When issues like mounting debt, life events such as marriage, childbirth and retirement, or the abuse of income on hopeful expenses like lottery tickets or gambling are at the forefront of employee focus, you can rest assured that they will jump at the opportunity to leave for greener pastures. This can add costly recruiting and onboarding efforts while disrupting the flow of production that may impact general employee morale.

As the labor market continues to tighten, employee benefits are becoming an important factor in the decision to join an organization. This includes the ability to save for retirement, but also having access to the education and tools to make informed financial decisions. Potential employees are more likely to be attracted to a company that cares about their financial well-being.

Pay it Forward

Financial literacy is at the forefront of many discussions across both professional and educational industries with programs designed to teach their audiences what they should be doing instead of addressing why they aren’t doing it. You may offer retirement benefits, an employee stock purchase plan, a HSA or FSA, and maybe even some equity sharing program but you still have employees who do not take advantage. Financial literacy may solve the how but doesn’t solve the why. Your employees may have experienced financial trauma that they just can’t seem to get past in order to make the right decisions with their money and because it’s a taboo topic they never discuss it.

Financial empowerment addresses the underlying issues that impact mindset and follow through behaviors at all levels of the business. That means that senior leaders and executives can not only address their own financial challenges, but can partner with those less senior and provide mentorship that helps prepare them to succeed as future leaders. These actions create an internal ecosystem that promotes holistic growth extending beyond political power and title, and into the factors that impact production, engagement, retention and representation aimed for through Diversity, Equity and Inclusion (DE&I).

Higher Margins

Workers that are unprepared for retirement will naturally need to work longer. As employees age, benefits costs for an organization will also increase in the form of higher health care costs, protection product premiums and salaries. By investing in a robust financial wellness program that enables employees to retire on their own terms, these costs can be greatly reduced.

Productivity and Engagement

While many organizations offer financial wellness programs, many employees are not participating in them. To implement a successful program, employers need to set a strategy, identify goals and objectives, utilize data and tools available from their provider and regularly communicate and educate their employees. Employees need a trusted source of guidance customized for individuals at both ends of the spectrum – those who are saving more and those grappling with serious financial issues. Increasing participation in a robust financial wellness program can reduce distractions and presenteeism, increase productivity and lead to engaged employees.

Where do we go from here?

The unfortunate combination of the pandemic and inflation has impacted both the availability of discretionary income to allocate toward retirement saving, but also future retirement income purchasing power. The need for robust financial wellness programs are now more important than ever. As a retirement consulting firm singularly dedicated to improving the retirement readiness of its clients, USI Consulting Group (USICG) can design a financial well-being program that addresses the unique needs of an organization by bringing together the capabilities of providers that are best aligned to your needs.

How USI Consulting Group Can Help

USICG’s team of experts is committed to delivering health, wealth and investment solutions to and through the workplace. To learn more about USICG’s solutions and how we can help implement a financial wellbeing program, contact your local USICG representative, visit our Contact Us page, or reach out to us directly at information@usicg.com.

This information is provided solely for educational purposes and is not to be construed as investment, legal or tax advice. Prior to acting on this information, we recommend that you seek independent advice specific to your situation from a qualified investment/legal/tax professional. 1022.S0609.99062

INSIGHTS BY TOPIC

Not receiving our newsletter?

Stay up to date with retirement plan updates and insights by subscribing to our email list.