Retirement Insights

Leveraging the Annuity Market to Secure Financial Stability

February 9, 2026

Over the past decade, pension plan sponsors have increasingly turned to the annuity market to reduce risk and stabilize their financial outlook. In fact, pension risk transfer (PRT) volumes hit record highs in recent years, with $41.5 billion in liabilities transferred in 20231 and $51.8 billion in 20242.

This surge has been driven by improved funded status from strong equity markets, higher interest rates that lower liability values and rising Pension Benefit Guaranty Corporation (PBGC) premiums that make maintaining plans more costly. Employers are also motivated by the desire to reduce balance sheet volatility and administrative complexity. Yet, a significant number of plans remain exposed, leaving sponsors vulnerable to market fluctuations and interest rate shifts.

The Window of Opportunity

Current market conditions present a rare chance for employers to secure favorable pricing and transfer risk efficiently. While annuity purchase rates generally track with interest rates for other investments of similar duration—such as the 10-year Treasury or 15-year mortgages—they are not identical. At the end of 2025, we are still seeing final annuity quote pricing north of 5%, which represents an attractive level compared to historical rates.

|

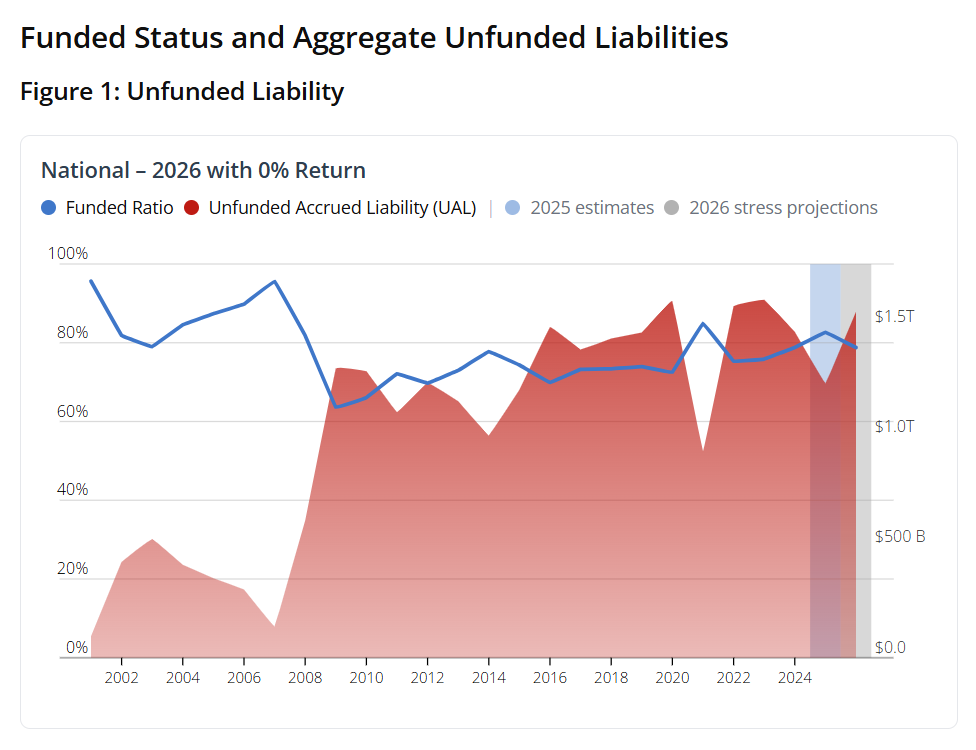

Figure 1 tracks the rise of public pension debt from 2001 through 2024, using market values for assets, with projections for 2025 and a stress test for 2026. The stress test applies either a 0%, -10%, or -20% market return in fiscal year 2026—pension funds experienced -20% during the Great Recession—to see how well today’s pension systems could weather another major market shock. Under the worst of these scenarios, the average funded ratio across U.S. pension systems would drop to 63%, revealing how vulnerable these plans remain to market volatility despite years of supposed recovery. The stress test is particularly important given how market crashes have historically had a major impact on pension funding that lasts decades.3 |

However, conditions are changing. The Federal Reserve cut rates three times in 2025 and signaled further reductions, which will directly pressure annuity pricing and lower guaranteed payouts. As insurers earn less on their investments, they will reduce crediting rates and lifetime income guarantees, making today’s rates a fleeting advantage.

The Risks of Waiting

Three converging factors amplify the urgency for sponsors:

|

|

|

| Historic stock market highs create vulnerability to a correction. A downturn could quickly erode funded status, reversing recent gains. |

Interest rate cuts by the Federal Open Market Committee (FOMC) increase the present value of liabilities. Lower discount rates mean higher obligations, making annuity pricing less favorable over time |

Pension trusts absorbing full-service costs strain plan resources. Rising administrative and compliance expenses add pressure to already tight budgets. |

Individually, these factors can chip away at financial stability. Combined, they could accelerate unfunded liabilities and increase volatility, leaving organizations exposed to risks that may be harder and more expensive to manage later. Acting now allows sponsors to lock in favorable annuity pricing and protect against these looming challenges.

Why Act Now?

- Lock in historically favorable annuity rates before further Fed cuts reduce guarantees.

- Protect funded status from potential market corrections and rising liability values.

- Avoid escalating PBGC premiums and administrative costs that strain plan resources.

- Secure long-term stability with a proven de-risking strategy while conditions remain advantageous.

Additional Strategic Actions Employers Should Consider

If your organization is not ready to move into the annuity market, there are still proactive steps employers can take to strengthen their financial position. Focus on optimizing operations, reducing costs and improving liability management now so your organization is prepared when market conditions align with your strategy.

|

Bundle services to reduce costs |

|

Streamline processes to eliminate redundancies and enhance operational efficiency |

|

Add online pension plan administration to take efficiency a step further. Digital platforms centralize plan data and provide participants with self-service access to estimate retirement benefits, statements, forms, and retirement kits—reducing the administrative burden on HR teams. This approach improves accuracy, accelerates response times and enhances participant experience by making information available anytime, anywhere. For employers, online administration means fewer manual interventions, stronger compliance controls and the ability to focus on strategic decisions rather than day-to-day paperwork. |

|

Position actuaries as strategic consultants in liability management and annuitization decisions. Actuaries should not only be involved in valuation but also in shaping liability management strategies. Their expertise in modeling interest rate scenarios, mortality trends and annuity pricing makes them indispensable for informed decision-making. By elevating actuaries to a strategic role, employers can better anticipate market shifts and optimize timing for annuity purchases. This proactive approach often results in lower overall liability costs and improved funded ratios. |

Whether an employer's goal is partial annuitization to offload a portion of liabilities or full plan termination, these steps create a foundation for resilience against market shocks and interest rate volatility.

The Bottom Line

Organizations who act now to engage the annuity market will secure pricing advantages and reduce exposure to economic uncertainty. Delaying action risks higher costs and fewer options as rates decline and market conditions tighten. In short, the cost of waiting could far exceed the cost of acting today.

How USI Consulting Group Can Help

Every plan is unique, and our goal is to help our clients make informed decisions that protect their organization’s future, while providing security for your employees.

USI Consulting Group provides access to single premium annuity contracts through leading insurance carriers, supported by objective analysis from experienced actuaries and annuity consultants. We work closely with you to evaluate the merits and limitations of annuity purchases for your specific situation. Our integrated approach goes beyond individual strategies, delivering cost savings, reducing volatility and improving long-term security. With expert guidance and a proven process, we help you confidently navigate complex de-risking decisions with ease.

Start the conversation today by visiting our Contact Us page or email us at information@usicg.com.

![]()

1 LIMRA Secure Retirement Institute 2023

2 LIMRA U.S. Group Annuity Risk Transfer Sales Survey 2024

3 Reason Foundation Annual Pension Solvency and Performance Report – Funding Health & Risk Assessment

Investment advice provided to the Plan by USI Advisors, Inc. Under certain arrangements, securities offered to the Plan through USI Securities, Inc. Member FINRA/SIPC. Both USI Advisors, Inc. and USI Securities, Inc. are affiliates of USI Consulting Group.

This information is provided solely for educational purposes and is not to be construed as investment, legal or tax advice. Prior to acting on this information, we recommend that you seek independent advice specific to your situation from a qualified investment/legal/tax professional. | 2126.S0126.99003

INSIGHTS BY TOPIC

Not receiving our newsletter?

Stay up to date with retirement plan updates and insights by subscribing to our email list.